Enter Decentralized Finance

Until very recently, financial transactions always required trusted intermediaries like banks, brokers, lawyers, etc. Historically, we have seen financial institutions take advantage of their privileged position: For example, banks can take on financial risks that their customers are ultimately on the hook for. The 2008 Recession was just the most memorable example, famously referenced via a Times headline (“Chancellor on brink of second bailout for banks”) in Bitcoin’s genesis block.

More than a decade after Bitcoin’s genesis block, we are seeing an entire alternative financial system built on top of blockchains. Decentralized finance (DeFi) is used as an umbrella term for financial services carried out on a blockchain. The trust provided by a shared ledger and automatic execution (“smart contracts”) allows anyone to do business without the need for middlemen. This entire financial ecosystem is not just open to anyone, but open-source, meaning the entire code can be copied and reused without permission.

Finance is not just becoming digital but has entered the open-source paradigm.

DeFi first blossomed on Ethereum, where presently more than $60 bn is locked in DeFi applications. Each DeFi application, or dapp, provides a specific financial service. On the outside, they have similar capacities to traditional financial use-cases, the differences being that no third party has control over the funds, and that applications are open-source.

In our view, it is the latter point that completely changes the competitive dynamics and the reason why DeFi will give traditional finance (TradFi) a run for its money.

Each DeFi application is effectively a “money lego” that is ready-at-hand for anyone to use, whether for building a better user interface or combining it with other money legos into a more complex use-case.

Note that this naturally limits the degree DeFi applications can extract value (in stark contrast to traditional finance): All fees are transparently visible, and since the entire application is open-source, anyone can just make a copy (“fork”) with lower fees, in case they get unfairly high.

In the following chapter, we review major money legos, highlighting how each improves on traditional finance, before elaborating on why the open-source structure of DeFi leads to an unstoppable flywheel of innovation.

Before we dive in, it is important to understand that all of this is still based on experimental technology, and using DeFi is risky and still inaccessible for most people. There are nuanced discussions to be had about the problems of DeFi (and blockchains, more generally), but that’s not what we set out to do here. Despite any limitations, we are convinced DeFi will ultimately bring about better and more open financial solutions fit for our global and connected world.

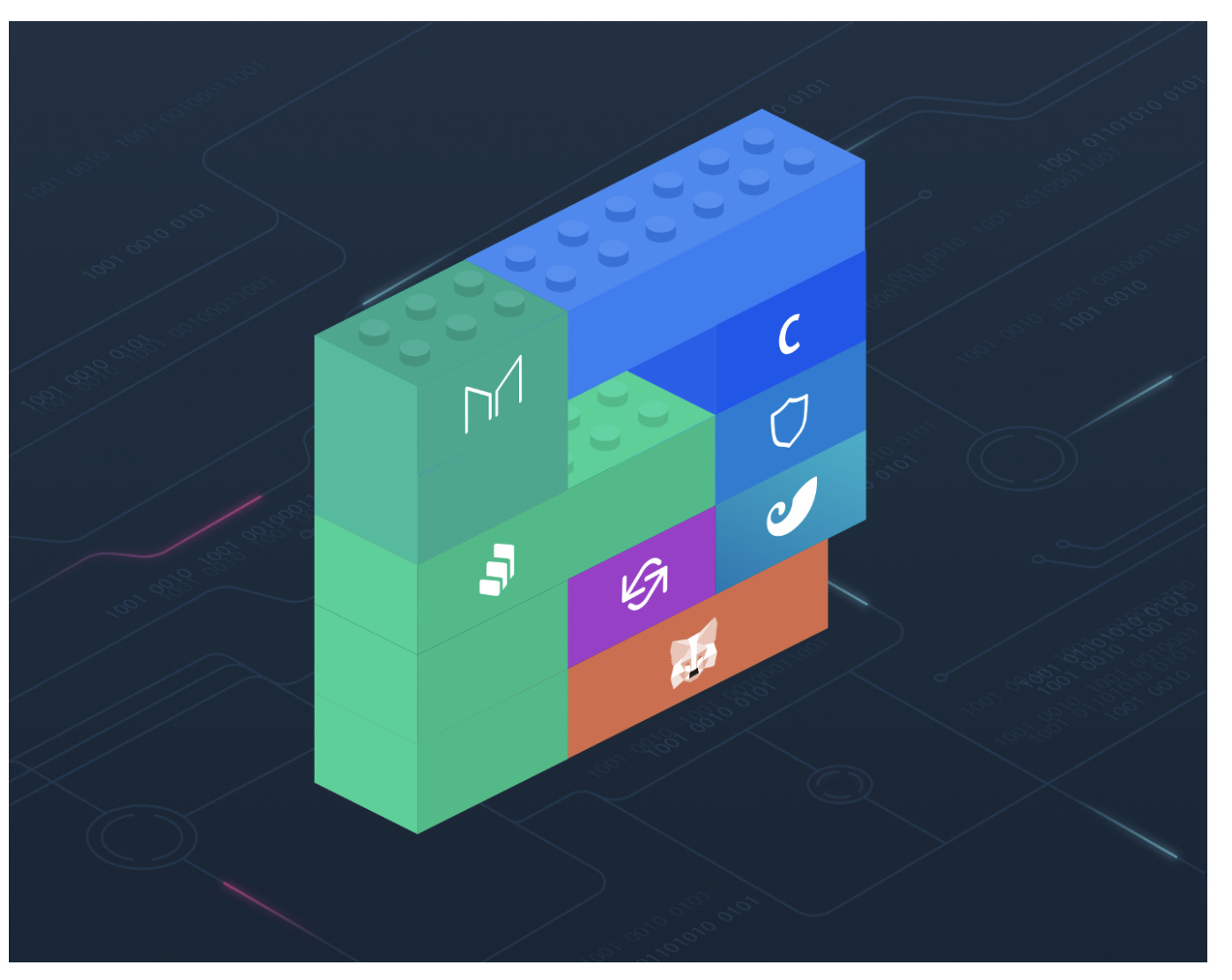

Overview of DeFi money legos

The “Decentralized” in DeFi points at the ideal to distribute control to the community of user-owners, who collectively shape the future of each application. Although decentralization often stays aspiration rather than reality, some projects that are entirely community-driven, like Yearn or Sushi, have made impressive strides over the last year.

DeFi dapps are non-custodial, meaning your assets are never managed by a middleman, like in the case of a bank or stock exchange. DeFi-powered services range from money exchanges, lending platforms, insurance providers, and many other financial services.

The reason why the pace of innovation in DeFi is so much higher than in traditional finance is because of the open-source nature of the Ethereum blockchain, and DeFi as a result. In stark contrast with the competitive logic of proprietary systems prevalent in “TradFi”, DeFi applications can be used, combined, and even copied by anyone without permission. The term “money legos” describes the fact that every application can be used freely as a building block for more applications.

Zerion provides a classic example: The dapp provides users with a high-yield bank account, allows them to invest in crypto assets, and even offers additional yield on these assets by lending them out to other users. Zerion can be accessed via a range of different Ethereum wallets and relies on three DeFi applications - MakerDAO, Compound, and Uniswap - to provide its functionality to users. The Zerion team didn’t have to build any of the “backend” mechanisms for swapping tokens, generating yield, etc. but could instead plug together existing money legos.

More examples can be found in this article by Totle, a decentralized exchange aggregator, building on a range of money legos themselves. Below, we list major money legos of DeFi and describe what they can do.

Stablecoins

Stablecoins are crypto-assets (typically Ethereum tokens) designed for stability. Amidst the extreme volatility of crypto, they may be the most crucial money lego to make DeFi relevant for financial services. Most stablecoins gain their stability through a peg to fiat currencies, typically the US Dollar, even though attempts at dollar-independent stability have launched (e.g. Rai).

There are different ways of achieving a peg to the US dollar, the simplest being to trust an entity to hold as many dollars as they give out stablecoins. Even though this method falls short of the crypto directive of not relying on trusted central parties, it has so far been the most prevalent way of issuing stablecoins, with leading examples such as USDT and USDC.

A more decentralized system is provided by MakerDAO’s Dai. Dai’s peg to the dollar is created through the MakerDao protocol, which offers loans in Dai against over-collateralized crypto. By loaning Dai only in exchange for a deposit of crypto collateral (for example, ETH) with a higher value than the loan, Dai is always backed by enough value. In case the price of the collateral drops below the allowed threshold, the crypto assets backing the loan will be auctioned off at a discount automatically. In this way, MakerDAO acts like a central bank of Ethereum.

Note the difference to how central banks, like the Fed, operate: The Fed prints US dollars which are not backed by anything at their own discretion, with little transparency or oversight. Anyone can issue Dai and create money with MakerDAO, but they back it up with more collateral to guarantee stability. Dai tracks the value of the USD but can be accessed by anyone with an internet connection. As a result, Dai has seen heavy traction in countries like Argentina, where accessing the dollar is more difficult.

Automated markets

Automated markets (AMMs) are the most successful model for so-called “Decentralized Exchanges”. They provide the same services as a currency or stock exchange does in traditional finance, but purely algorithmically and without any human control.

Uniswap, Ethereum’s largest Decentralized Exchange regularly exceeds the volume of Coinbase, the biggest “centralized” crypto exchange in the US. Comparing them illustrates the innovations of AMMs over traditional exchanges:

AMMs like Uniswap don’t need to pay staff to execute trades, have an office, or pay for registration, cutting most of the overhead normal exchanges face.

AMMs are uncensorable - traders can’t be stopped from accessing markets based on their country, income, etc.

Markets are available globally, 24/7, and on an equal playing field (all not true of stock exchanges, etc.).

AMMs allow anyone to earn trading fees by providing liquidity on distinct trading pairs (instead of the company running the exchange getting all the fees).

Synthetic assets

Synthetic assets are tokens that simulate the price of another asset, or any relationship between them. Projects like Synthetix employ similar collateralization mechanisms to MakerDAO in order to create tokens pegged to traditional assets, whether stocks, currencies, or commodities.

This provides a crypto-native way of getting exposure to traditional assets without ever holding them directly, and with all the benefits of crypto, like being open 24/7 to anyone. In this way, crypto users can now access stocks, commodities, and even indices.

Synthetic assets are an extremely powerful money lego to build more advanced instruments like leveraged exposure or custom ratios that would be hard to find on legacy trading platforms.

Money markets, Lending, and Yield Farming

Stablecoins and Decentralized Exchanges allow anyone to trade any crypto asset. The next set of money legos introduce ways of putting those assets to work. In DeFi, yields on stablecoins above 10% are seen commonly and even higher rates on volatile crypto assets.

Compound and Aave are among the leading lending services, with billions of dollars of value locked up in each of them. Lending protocols allow users to lend crypto assets or to borrow them, at interest rates set by market demand. Interest is gathered in real-time and often compounds automatically.

On top of that, some DeFi projects distribute their own token to users, adding to their yield. This new distribution mechanism is called “yield farming” - instead of selling tokens all at once, native tokens are distributed continuously to users, adding to their yield.

YEarn took things a step further and launched a protocol that continuously finds the best yields in DeFi and offers it to its users.

The powerful money legos of lending and yield farming open up the ability to earn yields orders of magnitude higher than in traditional finance to all Ethereum Dapps and users. What interest are you getting in your savings bank account? Chances are, it's a meager fraction of a percentage, while DeFi has been offering yields above 10% on USD for years. It’s not just cash that generates yield, but all kinds of assets can be lent to add interest on top of whatever price appreciation the investment ultimately achieves.

Flash Loans

Finally, we wanted to introduce a money lego that only exists in DeFi. Flash Loans, offered by Aave and others, are uniquely enabled by the architecture of blockchains. Flash Loans are loans that don’t require identification, credit checks, or even collateral because they are paid back within a single transaction block. Developers can borrow millions of dollars instantly and with zero collateral, as long as that liquidity is returned within the same Ethereum block. Most often, flash loans are used to take advantage of arbitrage opportunities. While it is profitable for arbitrageurs, their activity clears up price differences between different decentralized exchanges, making DeFi markets more efficient as a result.

Take-away: “TradFi” doesn’t stand a chance

As we explored with the specific money legos above, the global, interoperable, and open financial system of DeFi is a massive improvement from good ol’ TradFi:

DeFi has global and open currencies, not centrally controlled national currencies.

TradFi hosts trading venues which open only on weekdays from 9 to 5, and might just decide to block you from actually trading anyways, whereas DeFi has uncensorable 24/7 markets.

For everyone except the ultra-rich, interests in traditional finance rarely exceed a percentage a year, not even enough to cover for inflation. Yields in DeFi are orders of magnitude higher.

Any interesting investment within traditional finance can also be accessed in DeFi through synthetic assets while unlocking all the benefits of crypto tokens for that asset.

In each of the areas or money legos described above, DeFi has considerable advantages over TradFi and often provides 10x better solutions for users savvy enough to access them.

However, the real power of DeFi lies in its composability and interoperability: Every financial service within DeFi is available as a money lego for a more advanced application, or just as well the technical backbone for the newest competitor. Entry costs for new projects are extremely low and payoffs huge, while projects can’t build monopolies based on proprietary technology, lock-ins, and the other old tricks.

All of these factors combined result in a flywheel of innovation that will inevitably leave the financial dinosaurs of yesteryear in the dust.

We are already seeing Dapps assemble money legos into ever more complex use-cases that simply aren’t possible in TradFi. A recent example that will blow minds is Alchemix, which empowers people to take zero-interest, self-repaying loans against their future yield.

Financial services on DeFi are already more powerful than what legacy institutions can provide and we’re only just getting started. As its opportunities become more well-known, the user experience improves, and the flywheel of innovation keeps spinning, blockchains are bound to become the new infrastructure for global finance.